Last month, I received multiple emails from friends and clients on an interesting March 7 New York Times article (https://www.nytimes.com/2019/03/07/style/uber-ipo-san-francisco-rich.html) that considered the potential impact on San Francisco real estate prices when employees of these companies gain liquidity on stock options post-IPO. Shortly thereafter, a plethora of articles came out on the subject with respect to the SF real estate market. Below are links to some of these articles from publishers.

http://fortune.com/2019/03/08/san-francisco-housing-price-surge-expected-with-new-ipo-millionaires/

https://www.curbed.com/2019/3/19/18271522/san-francisco-real-estate-tech-ipo-airbnb-uber

https://techcrunch.com/2019/04/10/the-ipo-wave-of-2019-wont-upend-the-bay-area-housing-market/

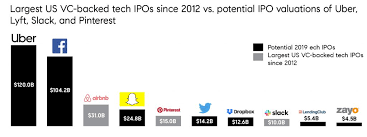

In the NYT article, 2019 projected IPOs include Lyft, Uber, Slack, Postmates, Pintrest and Airbnb. Lyft already went public on Friday, March 29, while Uber filed its S-1 on Thursday, April 11 and Pintrest just went public April 18. Articles are touting that “tens of thousands of employees” will be newly minted (multi) millionaires ready to spend their wealth of fast cars, expensive wines, Michelin-rated restaurants, and of course, real estate.

The emails sliced my thoughts and observations about the current local real estate markets. As a Realtor, I am asked almost daily what I think of the markets and whether real estate prices are trending up or finally cooling off. It has to at some point, right? Only in January 2018, I wrote a blog post on whether SF Bay real estate can sustain its growth trajectory. https://taosiliconvalley.com/2018/01/24/wow-what-a-strong-2017-in-terms-of-price-appreciation-and-stock-market-gains/

Every first time homebuyer in the last few years feared they were buying near the peak of the market. Regardless of that fear, all my buyer clients were ecstatic that they were now “in Bay Area real estate”. Although we all discuss real estate as an investment, a property also has the significant benefit of a certain lifestyle and place to start the next phase of life; it’s not pure financial decisions. With last month’s flurry of IPO articles, people’s view of near term future real estate prices have trended significantly more optimistic and seems to have assuaged much of buyer near term fears. But let’s dig a bit deeper than what these mainstream articles proclaim. Although directionally interesting, they don’t fully capture the nuances/details important in evaluating potential impact on the demand side of the equation. (https://taosiliconvalley.com/2013/08/26/microeconomics-101-for-real-estate-2/)

Just recently in 2nd half 2018, listings didn’t always sell in the 1st two weeks on MLS – some properties actually sold with no competition and some were taken off the market until the new year. Articles at that time questioned if this was finally the start of a market slowdown. We now know the answer – it has been a resounding “no”. Some data from late January came out in SF Chronicle. https://www.sfgate.com/business/networth/article/Bay-Area-housing-market-cools-but-it-s-still-13578433.php

My friends regularly ask my opinions on the SF Bay real estate and financial stock markets given my daily Realtor job, my BS/MBA in finance, and my former role as a start-up technology executive where I still keep up-to-date and have many high level connections in the industry. I have always tried to combine both my practical on-the-ground real estate knowledge with my previous analytical experiences to provide some directional and risk/reward/probabilities framework to friends and clients.

Before diving into some thoughts, note the following disclaimers: these are a) my personal ideas and not that of Coldwell Banker, b) high level overview and not a result of deep data analysis, c) recognize that the economy, stock market and thus real estate market can and do change very rapidly, d) commentary meant more to spur conversation rather than making any predictions, and e) a single macro-level trigger could shift the market rapidly and derail the IPO pipeline, economy and/or stock prices.

Articles on the SF IPO pipeline and its effect on the local real estate market somewhat over-simplify their analysis, and leave out several nuanced factors.

- There were many successful IPOs from recent years that did not garner the same headlines as this batch in 2019. The 2019 IPO pipeline contains many high profile consumer technology companies (Uber, Lyft, Pintrest, Airbnb, etc) compared with companies of past years which may have been more software, cloud, biotech and other less consumer recognizable names garnering less sensational news coverage. With that being said, this current crop does have some huge valuations historically unseen.

- IPOs are not the only form of liquidity events. Late stage venture funding and acquisitions are often liquidity events for founders, and early employees that are often unreported. For example, some early employees of Uber have already cashed out part of their options. https://www.pymnts.com/news/ridesharing/2017/uber-offers-longtime-employees-a-liquidity-event/. Others may have included a portion of their equity in a recent funding round. Most stock option grants have an accelerated vesting provision in a “change of control” situation. I have heard from my start-up and venture capitalist friends that more and more privately held companies want to remain private to avoid the scrutiny and higher costs as a public company, given the advent of significant capital available from late stage venture funds. Thus, some of the people who stand to gain with these IPOs may have already cashed out part of their equity earlier and already purchased real estate.

- A much smaller percentage of total reported full-time employees at these SF IPOs will see a “significant” cash windfall than what these articles purport:

- Options are vested over typically a 3-4 year vesting cycle. With a rapidly growing employee base, a large percentage of employees have less than 2 years of tenure.

- The more recently hired employees don’t receive as much stock options as earlier employees once companies gain traction and raise multiple stages of venture funding opting to pay competitive base salaries in lieu of big options grants. Majority of full-time employees will receive some options, and a liquidity event is something to celebrate and is meaningful, but may not be quite the impact that these articles purport.

- There is typically a 6-month lockout period post-IPO for employees. A lot can happen during that time. For example, Lyft went public on 3/29 and as of 4/19; their stock price dropped 19%.

- Although the companies such as Uber, and Lyft are SF based, their full-time employees are based all around the globe, so only a fraction of these employees are local. But yes, being headquartered in SF means that many of the executives and senior manager have some concentration in San Francisco.

- After a 6-month lockout, most employees do not suddenly cash out of their entire vested equity. Yes, some will sell a portion of their stock to purchase things or just to diversify their portfolio, but it’s not typically a sudden rush to sell it all when the lockout end. A blog post I wrote a few years ago talked a bit about my experience with lockouts and risk of illiquid in-the-money options. https://taosiliconvalley.com/2015/12/15/the-epic-story-of-unicorns-and-dragons/

- These articles discuss primarily the city of San Francisco real estate market. Only a fraction of those who work in San Francisco will want to buy in SF. Some will choose to buy in the Peninsula, and some will go to East Bay or Marin. Thus, the influx of people who now may qualify to purchase real estate or become move up buyers will not just be concentrated in the 47 square miles of beloved SF. Why?

- They can typically buy a more spacious property elsewhere outside city of SF.

- Cities outside SF have higher rated public schools – a very significant factor even if people don’t have kids yet.

- Those who choose to live in Peninsula (San Mateo county) want the flexibility in being in the midpoint between technology hubs in SF and South Bay. Silicon Valley is still the center of major high tech employers. Living in SF makes for a long commute to South Bay, even with the many company shuttle buses that pick up and drop off in various locations in San Francisco. https://www.citylab.com/transportation/2016/09/the-reach-of-the-bay-areas-tech-buses/500435/ Dual career households are commonplace nowadays for the young couples/families so having reasonable commute flexibility is paramount.

- Bay Area has fairly decent public transportation such as BART and Caltrain that allows people to live in East Bay or Peninsula and commute to SF.

- Discussion has been San Francisco companies based, but there are other Bay Area IPOs on the horizon that will have a cumulative affect driving higher demand too. For example, Zoom Video just went public on April 18 the same day as Pintrest. Zoom if based in San Jose which itself is seeing a surge of interest in downtown real estate. Rubrik, a Palo Alto based unicorn is also on the IPO horizon.

Start of 2019 has been very busy for me as Realtor and I have been active in different price ranges. I have had multiple listings and multiple buyers close escrow at the start of 2019. In each case where I represented the Sellers or the Buyers, there were 5+ offers in competitive situations.

We shall see what happens in Q4 this year and into Q1 2020 when companies who went public and have their 6 months lockouts expire. Will there really be an anxious rush to buy real estate driving up prices or will the market be able to more slowly absorb it into existing inventory over a longer period of time? In 2020, there is a macroeconomic factor – a Presidential election year. In 2016, there was a slowdown in real estate in both transaction volume as well as a small price decline from summer through the elections during a time of uncertainty. After the election, the stock market saw an uptick that also saw real estate prop up in the new year.

Regardless, even with all these additional factors that the popular news articles may not describe, the big SF IPO pipeline is a precursor to an increase in the demand-side of equation for nearby Bay Area real estate. The scale and level of impact that is the unknown. It’s also psychologically affecting both buyers and sellers on their motivation to buy right away, sell right away or wait. With strong job market, limited excess land to build new inventory, fantastic weather, close to mountains/ocean, cultural diversity and the center high tech, there is a reason why real estate is so fascinating and why prices are higher on $/square feet than most of US. There are near-term indicators of continued strong Demand while the Supply (listings) is limited; one must be aware that there are many factors that can affect short term valuation movements that the articles do not consider. As mentioned in previous blog posts, buying with a medium-to-long term horizon has proven for most to be a wise financial investment.

As always, please reach out to Peter Tao anytime if you wish to discuss anything real estate related at peter.tao@cbnorcal.com. Please like my FB page at https://www.facebook.com/PeterTaoProperties/ if you wish to get future posts or my upcoming listings.

Pingback: Go Niners…oh, and Initial 2020 Leading Indicators in SF Peninsula Real Estate | Tao SF Peninsula Real Estate